Risk-Based Approach: What it is, how it works, and why it matters

- azakaw

- Feb 28

- 17 min read

Updated: Jul 16

Compliance officers traditionally saw their role as checking off a list of tasks. They assumed meeting specific regulatory requirements was enough to avoid legal trouble. But today, such a strategy no longer makes sense.

That's why institutions and compliance officers are turning towards a more effective strategy: a risk-based approach.

In this article, you'll learn how a risk-based approach works, from the key elements and implementation to the benefits to your business.

Risk-Based Approach (RBA) Key Takeaways |

|

|

|

|

|

|

|

|

|

|

|

What Is a Risk-Based Approach?

A risk-based approach is a compliance program that allocates resources based on risk levels. It focuses most intently on transactions or relationships that are likely to involve financial crimes, such as money laundering.

This approach customizes monitoring and due diligence for each client. Institutions use data from past experiences, trends, and other factors to guide decisions.

This allows them to respond more effectively to suspicious activity and to prevent problems before they happen.

What are the benefits of an RBA in AML compliance?

A risk-based approach has several benefits in AML frameworks because:

Improves the detection of suspicious activity;

Reduces false positives;

Optimises compliance resources;

Enables faster customer onboarding;

Strengthens audit and regulatory outcomes;

Supports business scalability;

Provides better risk-driven decision-making across the organisation.

More effective detection of suspicious activity

In a rule-driven environment, monitoring thresholds and controls are often applied uniformly. This generates large volumes of alerts, many of which relate to low-risk customers, making it harder for compliance teams to identify genuinely suspicious behaviour.

A risk-based approach changes this dynamic. Higher-risk customers and activities are subject to enhanced monitoring, while lower-risk relationships are handled through simplified controls.

This allows AML compliance teams to focus on higher-value cases, improving detection rates and the overall quality of alerts.

Optimised use of compliance resources

Compliance teams operate under constant pressure to manage growing volumes of transactions, customers, and regulatory expectations. Applying the same level of scrutiny to every relationship leads to inefficient use of time and budget.

With a risk-based model, resources are allocated where they have the greatest impact:

High-risk areas receive deeper analysis and more frequent review;

Low-risk segments require less manual intervention.

This reduces investigation backlogs, lowers operational costs, and improves team productivity.

Faster and more proportionate customer onboarding

Customer experience has become a critical factor for banks, fintechs, and digital asset firms.

A risk-based approach enables simplified due diligence for low-risk customers and enhanced due diligence only where it is truly needed.

This shortens onboarding times without increasing exposure to financial crime and ensures that compliance controls remain proportionate to the risk presented.

Related content: What is digital customer onboarding?

Stronger regulatory outcomes and audit readiness

Supervisory authorities increasingly assess not only whether an institution has an AML framework in place, but whether its controls are demonstrably risk-driven.

After years of working with AML compliance, our team knows that a mature risk-based approach provides a clear link between:

The enterprise-wide risk assessment

Customer risk scoring

Monitoring scenarios

The level of due diligence applied

This traceability strengthens audit outcomes, reduces regulatory findings, and demonstrates that the institution understands and actively manages its financial crime risk.

Scalability as the business grows

As institutions expand into new products, channels, and jurisdictions, AML programmes must scale without a proportional increase in manual workload.

A risk-based model supports this growth by segmenting customers and activities according to risk and applying differentiated controls.

This allows organisations to onboard more customers, process higher transaction volumes, and enter new markets while maintaining effective financial crime controls.

Better decision-making across the organisation

A risk-based approach is not only a compliance tool; it is a decision-making framework.

Risk insights support strategic choices such as entering new geographies, launching new products, defining risk appetite, or accepting higher-risk customer segments.

This elevates AML from a reactive control function to a proactive component of business strategy.

Why do regulators require a risk-based approach?

It's impossible to identify every instance of money laundering or terrorist financing. Therefore, regulatory bodies now believe institutions should be more proactive than simply checking compliance forms.

A risk-based approach is required because it enables institutions to:

Demonstrate a clear understanding of their risk profile: Firms must show that they understand their customers, products, services, delivery channels, and geographic exposure, and how these elements influence their financial crime risk.

Allocate resources where they have the greatest impact: A one-size-fits-all model wastes time on low-risk relationships and reduces the attention given to higher-risk customers and activities. A risk-based approach ensures enhanced scrutiny is applied where it is truly needed.

Reduce unnecessary compliance burden without increasing exposure: Low-risk customers can go through simplified due diligence, enabling faster onboarding and better customer experience, while high-risk customers are subject to enhanced controls.

Apply proportionate and effective controls: Regulatory expectations are based on proportionality. A student opening a basic account does not present the same risk as a multinational company operating in high-risk jurisdictions, and the level of due diligence must reflect that difference.

Maintain an effective AML framework despite limited resources: Budget, technology, and human resources are always finite. A risk-based model ensures they are used in the most efficient and defensible way.

How the Risk-Based Approach works

If you're going to use a risk-based strategy, you need a plan, and everyone in your organisation has to follow it religiously.

This plan must start with a thorough examination of your data (a process known as AML risk assessment), because everything you do to mitigate risk will be based on what you find out during this initial assessment.

Your plan should also include ways to update your risk assessment on a regular basis, since both the types and levels of risk can change over time.

Here are the individual components that make up a successful risk-based approach, and why each one is important for your business:

Identifying risks

The first thing you have to do is figure out where on your product or service menu, and in which of the countries where you do business, money laundering might pose the greatest risk.

You're looking for vulnerabilities here: places where a determined launderer might be able to sneak past your defenses.

Assessing and prioritising risks

Once you've got a good idea of what your vulnerabilities are, it's time to prioritise them. You do this by ranking the risks you've identified in terms of how serious they are.

For example, if there is a particular type of transaction or customer that has more potential than others, you would give it higher priority when deciding which controls might be most effective in reducing or managing that specific kind of risk.

Applying proportionate controls

After prioritising your risks, the next thing to do is apply controls that take into account both their level of severity and the likelihood of something going wrong (in other words, their "risk score").

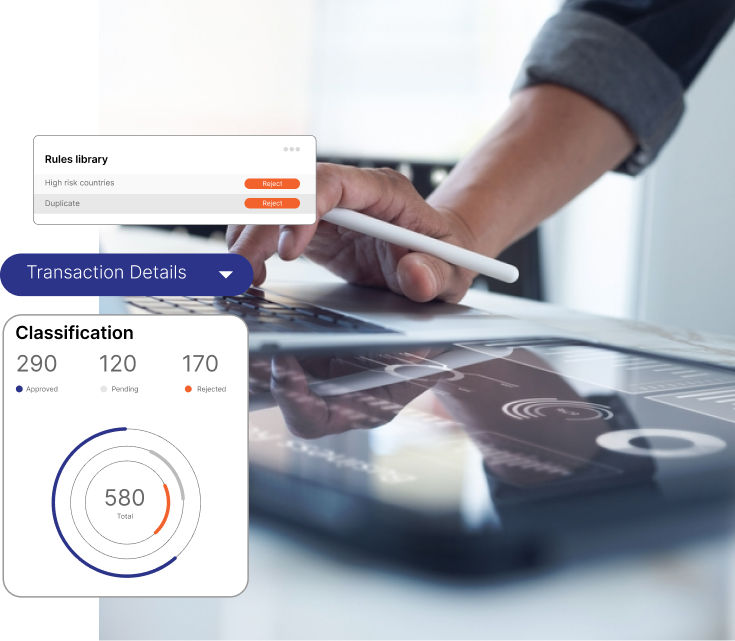

One way banks and financial institutions do this is by using an automated system to give customers a risk rating. They can then use these ratings when making decisions about whether someone poses too great a money-laundering threat.

Effortless Bank Compliance Software

azakaw automated customer risk rating allows you to deliver exclusive banking services without compromising on stringent compliance requirements.

Ongoing monitoring and review

Because new risks are constantly emerging as old ones change or disappear, this process doesn't just happen once; it's ongoing.

You also need to keep tabs on existing customers and update your overall risk assessment frequently so it always reflects current circumstances.

What a risk-based approach looks like in real operations

In a fully operational environment, the risk-based approach is visible across the entire customer lifecycle.

Low-risk → simplified due diligence

Medium-risk → additional verification

High-risk → EDD + senior review

In transaction monitoring:

Thresholds calibrated by risk

Alerts prioritised by risk score

According to our experience and expertise, without this, the RBA is only a documented policy.

TIP: Read our article "Synthetic Transaction Monitoring" to learn how it's related to RBA in AML compliance.

Applying proportionate controls

When controls are not aligned with risk:

Low-risk customers are over-reviewed

High-risk activity is diluted

Investigation backlogs increase

Compliance costs rise

Risk-Based Approach in AML Compliance

The risk-based approach is a widely accepted best practice in AML compliance worldwide. In fact, it's often referred to as "the cornerstone" of an effective AML compliance programme.

What is the AML risk-based approach?

In AML circles, this method is used to identify, assess, and mitigate the risks associated with money laundering and terrorist financing.

By employing a risk-based approach, institutions are better equipped to detect and prevent suspicious activity at an early stage.

As well as screening customers prior to onboarding them, financial institutions and other businesses also need to monitor their transactions regularly for any unusual patterns that could indicate dirty money.

Related content: Financial crime prevention

Who needs to adopt a risk-based approach?

Any organisation subject to AML/CTF obligations must adopt a risk-based approach. This includes banks, fintechs, payment service providers, crypto-asset firms, venture capital firms, asset managers, and other regulated businesses.

The level of sophistication will vary depending on the size, business model, and geographic exposure of the institution, but the underlying principle remains the same: controls must be aligned with risk.

Read also:

How FATF defines the risk-based approach

According to FATF, "you cannot fight what you do not understand."

In other words, if you don't have a good grasp on your specific risks, you can't take effective measures to counter them.

This is why it's crucial to identify and understand your risks first, so you can then develop strategies for mitigating or managing them.

For instance, by understanding which of your products pose higher risks of money laundering, or in which countries these risks may be greater.

What are the key risk factors in a Risk-Based Approach?

The key risk factors in the RBA approach are: customer risk, product and service risk, geographic risk, and delivery channel risk.

When you are determining risk, it is important to know what you are looking for and where. While various factors contribute to risk, these are the four main areas of risk that every business should pay attention to get an accurate risk assessment for their AML purposes.

Customer risk

There are different AML customer types, and not all customers are created equal from a risk standpoint. Certain individuals, like politically exposed persons (PEPs), represent a higher risk to your business than others do and, as a result, require extra scrutiny.

You must know who your customers are and what their occupations are, as well as other pertinent information like their source of wealth.

Know Your Customers Like No One Else

Go deeper than standard KYC with dynamic risk profiling, sanctions and PEP screening, adverse media monitoring, and AI-powered risk scoring. Learn how azakaw’s intelligent compliance engine lets you gain full visibility from day one.

Product and service risk

Just like some customers are riskier than others, some of your products or services can be more appealing to criminals who are trying to launder money.

Anonymous prepaid cards and other products that can be used without being traced are a high risk for AML purposes.

In addition, high-risk transactions such as high-speed transactions need to be scrutinized more closely.

Geographic risk

The country that your business is located in, as well as the countries where you do business, can also pose certain risks. Countries with weak AML laws and regulations can be a breeding ground for money laundering.

It is important to stay up to date with the current high-risk countries and keep this information on file.

FinCEN and the FCA keep an updated list that you can refer to when you need to determine geographic risk.

Secure & Scalable AML Compliance

Address the distinct compliance needs across multiple jurisdictions with custom AML compliance templates with azakaw, an AI-powered tool that prevents money laundering and financial crimes.

Delivery channel risk

How your clients do business with you can also be a risk factor to consider.

Channels with less personal interaction, like online channels, can be a higher risk than traditional channels where customers interact with your business on a personal level.

What is the difference between the Risk-Based Approach and traditional compliance models?

The key difference is that a rule-based model applies the same controls to every customer, while a risk-based approach adjusts due diligence, monitoring, and reviews according to the level of financial crime risk.

Traditional compliance frameworks rely on static rules and checklists. A risk-based approach, by contrast, is dynamic and allocates resources where the risk is highest.

Rule-based compliance | Risk-based approach |

Applies uniform controls to all customers | Applies proportionate controls based on risk |

Static thresholds and monitoring scenarios | Monitoring intensity calibrated by risk level |

High volumes of low-value alerts | Prioritisation of higher-risk activity |

Limited flexibility | Adapts to new typologies and emerging threats |

Focus on formal compliance | Focus on effective risk mitigation |

Limitations of one-size-fits-all controls

In traditional AML compliance models, every customer or situation is treated the same, regardless of their individual circumstances and risk profile.

This often leads to:

an excessive number of false positives, which overload compliance teams;

false negatives, where genuinely high-risk activity is not detected;

unnecessary friction for low-risk customers.

How to implement a Risk-Based Approach

While there are many benefits to risk-based AML compliance, implementing this type of model requires commitment from the top down as well as a significant investment in technology and personnel.

Once you have committed to a risk-based approach, you need to build a culture that supports this model, including ongoing training for all employees and investment in the right technology.

1. Establishing a risk governance framework

A clear governance structure is essential to ensure ownership and accountability. It must be founded on a solid organizational framework that outlines:

The roles and responsabilities and duties of all stakeholders.

Senior management oversight;

Approval and review processes for risk methodologies.

This framework must be documented, communicated, and commonly understood throughout the organization.

2. Performing enterprise-wide risk assessments

No AML compliance program is complete without an enterprise-wide risk assessment. It provides a structured view of the institution’s exposure to financial crime by evaluating:

Customers

Products and services

Delivery channels

Geographic footprint

This assessment must be documented, regularly updated (annually, at least), and directly linked to the controls applied in practice.

3. Designing the customer risk scoring methodology

Institutions need a consistent and auditable way to classify customers according to risk. This requires:

Defined risk factors

Clear scoring logic

Documented risk thresholds

Rules for triggering enhanced due diligence

The methodology must be explainable to auditors and regulators.

Read also: Inherent risk vs residual risk

4. Designing proportionate controls

The next step in your AML compliance program is to develop specific controls that are proportionate to your overall risk level.

Implementation is only effective when the defined risk levels drive real operational outcomes.

This means:

Onboarding workflows must change based on risk

Monitoring scenarios must be calibrated by risk category

Review frequency must reflect the customer’s risk profile

Data analytics plays a central role by helping you understand where money laundering might most likely occur, and which rules and thresholds will most effectively prevent this crime.

5. Enabling the model through technology and data

Technology plays a central role in ensuring consistency and scalability. Key enablers include:

Automated risk scoring

Integrated KYC and transaction monitoring systems

Reliable and complete data sources

Poor data quality will undermine even the most sophisticated risk methodology.

The End-to-End Platform

Streamline compliance from risk scoring, KYC to corporate compliance and AML transaction monitoring, reducing costs and complexity so you can scale with confidence.

6. Embedding the risk-based approach into operations

For an AML compliance program to be successful, it needs to be more than just a set of rules and procedures. It also needs to be part of the day-to-day workflow.

The model must also generate a clear audit trail demonstrating how risk-based decisions are made.

Consequences of weak RBA implementation

If your risk assessment is wrong, then you are at risk of leaving your "front door" open to financial criminals.

The potential consequences for both firms and individuals can be severe, from large fines to being closed down by regulators.

Regulatory findings and supervisory criticism

An AML risk assessment is crucial in preventing money laundering and terrorist financing.

Supervisory reviews increasingly assess whether the risk-based approach is actively driving day-to-day controls or exists only as documentation. If there are weaknesses in this process, examiners will likely find them when they visit.

Their report could include a public censure of the bank and require it to undertake expensive additional audits.

In more severe cases, institutions may face:

Remediation programmes,

External lookback exercises,

Appointment of independent monitors.

This could also damage the bank's relationships with other financial institutions, including correspondent banking partners.

Inaccurate risk scoring and misclassification

Where financial institutions have incorrectly classified high-risk customers as low risk, this creates an opportunity for money launderers that may go undetected until a regulatory review.

In practice, this also means enhanced due diligence is not applied, monitoring scenarios are not properly calibrated, and higher-risk activity is mixed with large volumes of low-risk alerts.

Weak controls built on flawed assessments

A financial institution's anti-money laundering controls are based on its assessment of the risks it faces.

If this assessment is flawed, then so are its controls. There is, therefore, a danger that the institution will have a false sense of security about its ability to prevent and detect money laundering.

At the same time, this means that review cycles, onboarding decisions, and monitoring thresholds, in other words, AML controls remain misaligned with the actual risk exposure.

TIP: Read our ultimate guide to know everything about anti-money laundering

Audit failures and remediation costs

Audit failures can have very costly consequences, with financial institutions having to pay millions of dollars to fix the problems identified.

These remediation efforts often involve large-scale customer file reviews, reclassification of risk levels, redevelopment of risk models, and the use of external advisory support and new technology.

In some cases, they may have to bring in outside experts to do this, which can lead to a significant overhaul of their anti-money laundering and compliance programmes.

Challenges when applying a Risk-Based Approach

The implementation of a risk-based approach can be complex. There are some challenges that firms must overcome if they are to do this successfully.

Inconsistent risk scoring

Individuals undertaking risk scoring must do so consistently, but this can be challenging in practice, particularly in larger teams.

The differing opinions of team members can lead to confusion as to who poses a higher risk, resulting in manual overrides, inconsistent onboarding decisions, and reduced trust in the risk model.

Over- or under-application of controls

A risk-based approach requires firms to apply AML controls that are proportionate to the level of risk they have identified. The difficulty here is in knowing when too much or too little has been done.

Applying too many controls may deter legitimate customers and make it difficult for compliance teams to focus on higher-risk situations, while applying too few leads to monitoring gaps, ineffective enhanced due diligence, and increased regulatory exposure.

Read also: How do you check if a company is legit?

Documentation and audit challenges

Regulators expect not only that firms will take a risk-based approach, but also that they can demonstrate it.

They will need to keep detailed records of their risk assessments and of their decisions on how to manage risk, including a clear audit trail showing how risk scores influence due diligence, monitoring scenarios, and review frequency.

In fragmented technology environments, this traceability is often difficult to evidence, especially when AML data is spread across multiple systems.

How technology supports a Risk-Based Approach

While financial institutions face many challenges when implementing a risk-based AML approach, technology is available to help them overcome them.

By providing a framework for risk assessments and ensuring their consistent application, technology can play an important role in the success of any anti-money laundering programme.

Automated risk scoring

One major benefit of new technology is that it can do things much faster and more accurately than humans.

In particular, it has become very easy to use computer systems to give risk scores. This involves scanning a huge number of databases and coming up with a figure based on the information found.

Do you want to automate risk scoring?

Discover how azakaw helps you scale securely with automated risk scoring and transaction monitoring, reducing complexity, lowering costs, and strengthening compliance.

Dynamic and real-time risk assessment

Fraud detection has moved on from a simple tick-box exercise. Risk assessment must now be dynamic; that is, changing as circumstances alter.

For example, it's essential to flag up changes in customer behaviour in real time.

Data-driven decision-making

The best fraud detection strategies are data-driven. There's no room for guesswork or hunches. Instead, financial institutions need solid information on which to base their decisions.

Sophisticated data analytics can reveal patterns that might indicate new fraud types, an important aid in the fight against financial crime.

Regulatory expectations around the Risk-Based Approach

Supervisors assess not only whether a framework exists, but whether it is demonstrably effective in practice and actively drives day-to-day controls.

To avoid being fined or even losing their licences, financial institutions need to understand exactly what regulators are looking for and make sure they comply with all relevant laws and guidelines.

FATF guidance and global standards

FATF's recommendations outline the universal AML/CFT framework, which almost every country has adopted.

Key components of this framework include customer due diligence, monitoring for suspicious transactions, and reporting suspicious activity. Compliance with this standard is a top priority.

In particular, FATF Recommendation 1 requires institutions to identify, assess, and understand their risks and to apply controls that are proportionate to those risks.

National regulators and supervisory expectations

Even though the FATF recommendations provide a universal framework for AML/CFT, local regulations vary significantly across countries. It is crucial to understand all local laws and regulations wherever you're operating.

As a result, businesses operating in multiple countries are required to maintain a separate risk-based approach for each jurisdiction in which they operate.

Regulators expect institutions to demonstrate their use of the risk-based approach and to regularly prove its effectiveness.

In the MENA region, regulators such as the UAE Central Bank, ADGM FSRA, DFSA, SAMA, QCB, CBB, CBK, and the Central Bank of Oman have significantly increased their supervisory focus on the practical implementation of risk-based AML frameworks, particularly for banks, fintechs, and virtual asset service providers.

You may be interested in:

What regulators look for in practice

Regulators will review a business's records to ensure that its stated risk-based approach is being used on a day-to-day basis.

In addition, regulators want evidence that the institution has an effective risk governance framework in place and that its senior management team oversees risk and compliance activities.

In practice, supervisory reviews typically assess:

The methodology behind the enterprise-wide risk assessment;

How customer risk ratings are calculated and updated;

Whether monitoring scenarios are calibrated according to risk levels;

The consistency of onboarding and enhanced due diligence decisions;

The existence of a clear audit trail showing how risk scores influence controls;

Board and senior management oversight of the AML risk framework.

In MENA jurisdictions, these elements are frequently tested during on-site inspections.

In these inspections, institutions must demonstrate that their risk-based approach is embedded in daily operations rather than existing only in money laundering policies and documentation.

FAQs about the risk-based approach

What is the purpose of a risk-based approach?

The main objective is to fight crime more effectively while managing compliance costs.

What are the 4 pillars of a risk-based approach?

The four pillars of this approach include risk identification, risk assessment, risk mitigation through ongoing monitoring and review.

Is a risk-based approach mandatory?

Yes, it is. The majority of regulators around the world require financial institutions to adopt a risk-based approach.

How does a risk-based approach differ from risk management?

Risk management refers to a broad set of policies, procedures, and controls designed to identify and mitigate threats to an organization. A risk-based approach is a type of risk management, but one that is specifically designed to meet AML/CFT requirements.

Can a risk-based approach be automated?

Yes. Although some tasks within the risk-based approach will always need to be performed manually (such as complex decision-making), many can be automated using modern technology.

In fact, automating certain functions makes the risk-based approach stronger and more effective. For example, AI-powered screening and scoring systems can identify risks more accurately and reliably than human reviewers.

Conclusion

Transitioning from a conventional tick-box compliance practice to a risk-based approach gives your financial institution a competitive advantage.

This approach enables you to fight financial crimes while keeping customers satisfied and safe.

Understand that this is a journey, not a one-stop destination. Continuous learning and adaptability are therefore needed to confront new challenges and implement new AML compliance requirements.

If you are interested in establishing a risk-based compliance program for your financial institution, you are in the right place.

Our AML expert consultants at azakaw are available to assist you with their expertise. They provide the support you need and help you choose technological solutions that best suit your needs.

Related articles